- Home

- SBLC Issuance

SBLC Issuance

A Standby Letter of Credit as a Means of Payment

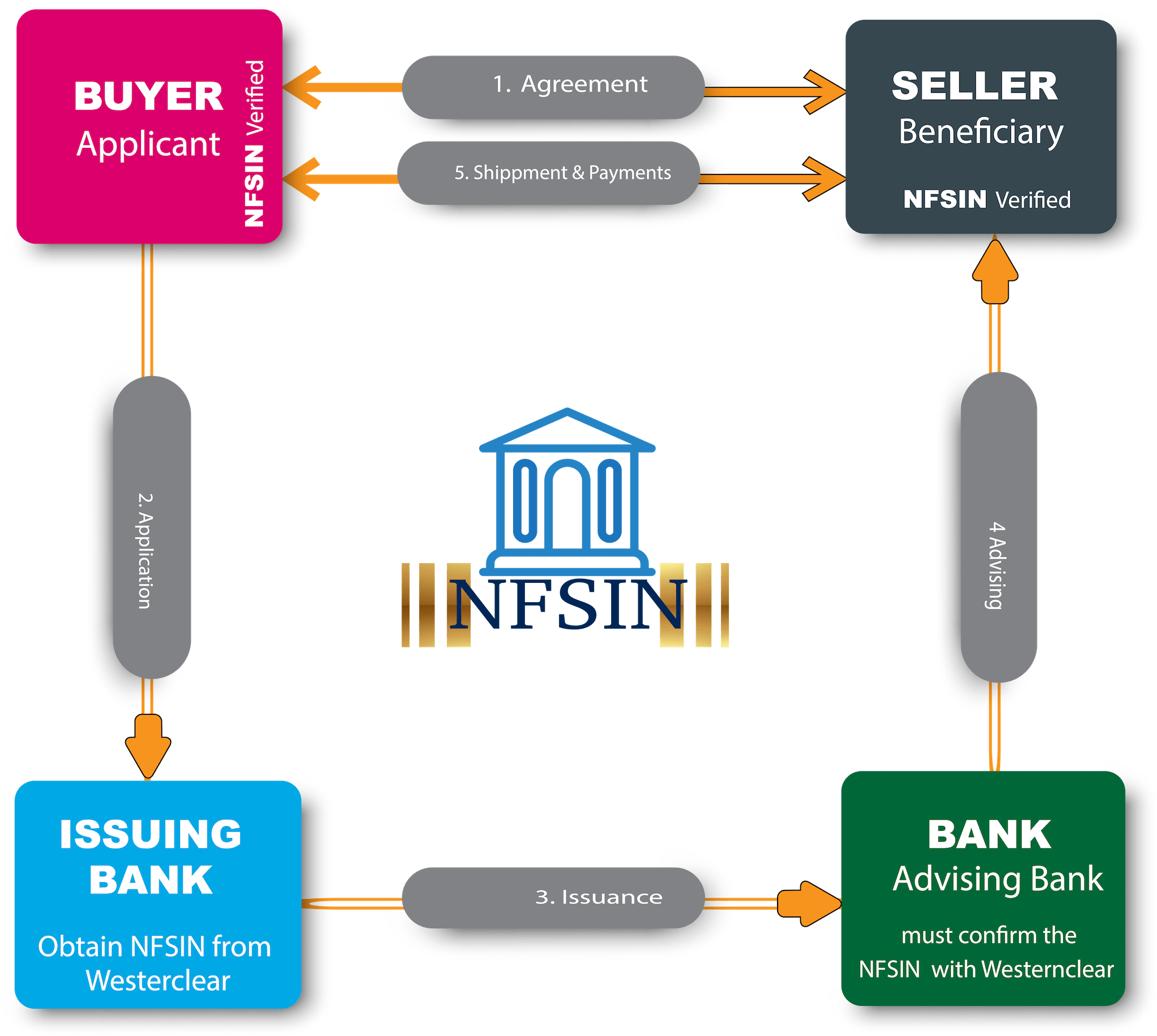

An SBLC instrument is utilized to underwrite domestic and international trade deals. It is a payment of the last resort and is used when the seller/exporter feels the buyer/importer may have problems paying for goods received.

If a seller feels the buyers credit rating is not good enough, they will ask for a Standby Letter of Credit. The buyer will request their bank to open a SBLC in favour of the seller. The seller will then ship the goods to the buyer.

If the buyer pays the seller, the SBLC is cancelled and returned to the issuing bank. If the buyer fails to pay, the seller will claim the sum owed against the Standby Letter of Credit. The issuing bank will pay the seller and claim the same from the buyer.

Want to know more about our services?

When an SBLC is monetised, it acts as a guarantee of payment. The verbiage within will exactly mirror that of a Demand Bank Guarantee. Both instruments will be governed by ICC Uniform Rules for Demand Guarantees, (URDG 758). They will be payable on first demand.

If a company is looking for a loan or line of credit, they can obtain a SBLC “lease”. They may “lease” a Standby Letter of Credit from a SBLC provider. SBLC Providers can be found in many countries including here in Geneva.

The lessee or beneficiary will sign a contract with the SBLC Provider. This contract is referred to as a COLLATERAL TRANSFER Agreement. The beneficiary will usually “lease” the Standby Letter of Credit from the SBLC Provider for one year.

The beneficiary will pay a Collateral Transfer Fee to the SBLC Provider representing the “Leasing” fee. The SBLC provider will instruct their bank to transmit the SBLC to the beneficiary’s bank. Upon receipt the beneficiary can offer their bank the SBLC as collateral for a line of credit or loan.

What is the SBLC Funding Process?

What is meant by the Standby Letter of Credit (SBLC) funding process? It means SBLC financing or monetisation. In other words, obtaining loans and lines of credit using a Standby Letter of Credit as collateral.

It must be remembered that a Standby Letter of Credit is also a major financial instrument that underpins global trade. It is utilised as a payment of the last resort. When used for international and domestic trade purposes a Standby Letter of Credit is not “leased”.

If a company wishes to obtain a loan or line of credit they will have to “lease” a Standby Letter of Credit. This they can do from a SBLC provider as explained below.

Who is an SBLC Provider?

Explaining the ‘Leased” Standby Letter of Credit or SBLC ‘Lease” Process

-

Access to a large direct investor base our client franchise comprises over 2,000 financial institutions in over 90 countries

-

Access to a large direct investor base choose from approximately 50 settlement and 100 denomination currencies, as well as multiple instrument types and applicable legal jurisdictions

-

Dedicated expert support our experienced support teams guide you throughout the issuance process

-

Same-day distribution efficient distribution of securities to investors on the same day as issuance

-

Increased transparency shareholder and bondholder identification services give you a clear overview of your investors